CHEVRON (CVX)·Q4 2025 Earnings Summary

Chevron Posts Record Production as Earnings Fall on Weak Oil Prices

January 30, 2026 · by Fintool AI Agent

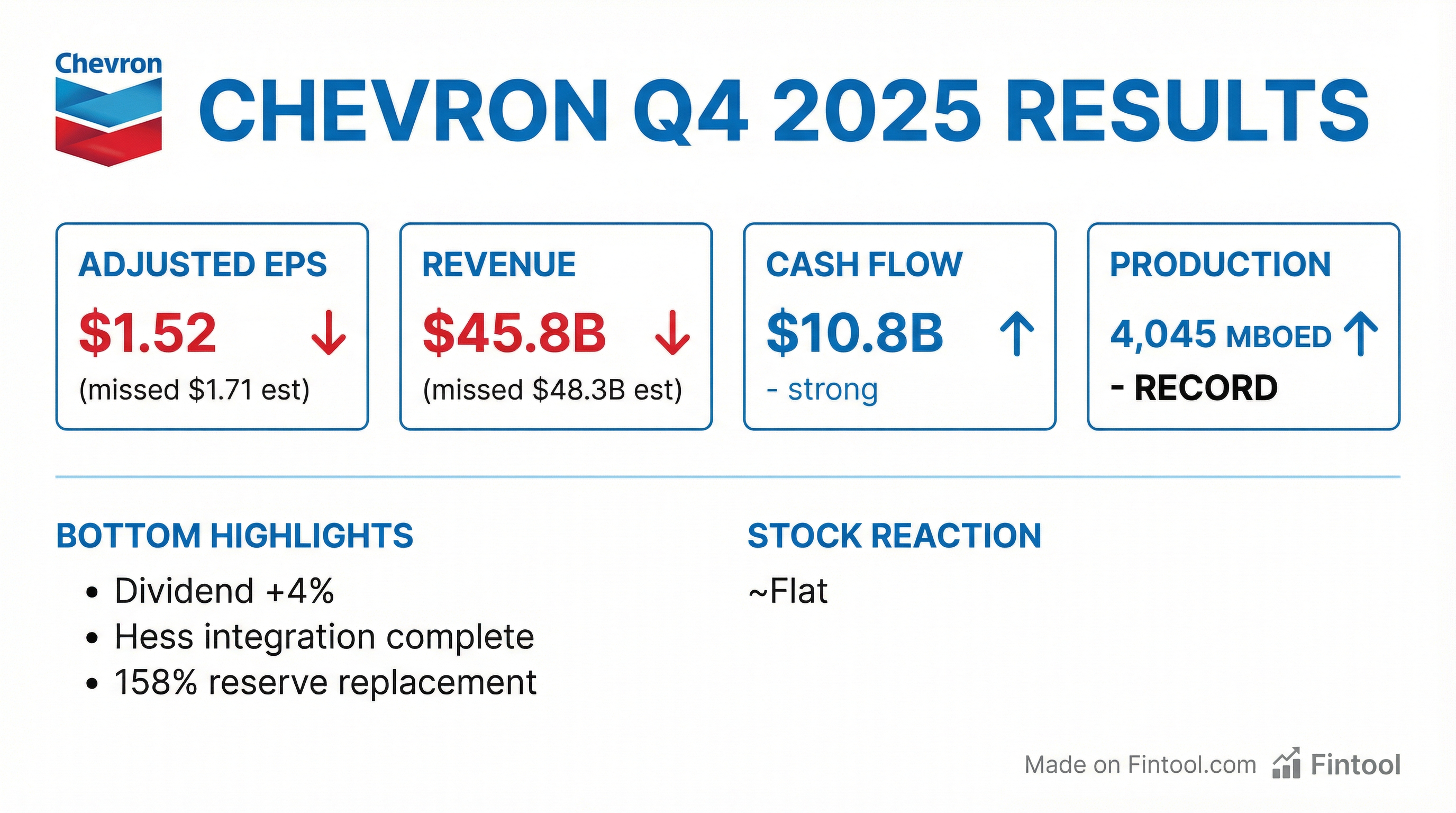

Chevron reported Q4 2025 adjusted earnings of $3.0 billion ($1.52 per share), down from $3.6 billion ($2.06 per share) in Q4 2024, as lower crude oil prices more than offset record production levels and successful integration of the Hess acquisition.

CEO Mike Wirth struck a positive tone despite the earnings decline: "2025 was a year of significant achievement. We successfully integrated Hess, started-up major projects, delivered record production and reorganized our business. This resulted in industry-leading free cash flow growth and superior shareholder returns, despite declining oil prices."

The company raised its quarterly dividend 4% to $1.78 per share, extending its streak of annual dividend increases to 39 consecutive years.

Did Chevron Beat Earnings?

Chevron's Q4 2025 results reflect the challenging commodity price environment:

The earnings decline was driven primarily by:

- Lower crude prices: Brent averaged $64/BBL vs. $75/BBL in Q4 2024

- Unfavorable foreign currency: Decreased earnings by $130 million

- Lower affiliate earnings: Primarily at Tengizchevroil

Partially offsetting these headwinds were higher refined product margins and increased sales volumes from the Hess integration.

What Changed From Last Quarter?

Production hit new highs. Worldwide net oil-equivalent production reached a record 4,045 MBOED in Q4 2025, up 21% from 3,350 MBOED a year ago.

U.S. production growth was driven by:

- Hess acquisition contribution

- Gulf of America deepwater project startups (Anchor, Ballymore, Stampede, Whale)

- Permian Basin growth to 1 million BOE/day

International production gains came from:

- Hess assets, primarily Guyana

- TCO ramp-up in Kazakhstan to ~1 million BOE/day

- Offset by asset sales in Canada and Republic of Congo

How Did the Stock React?

Chevron shares traded essentially flat following the earnings release, closing at $171.19 (+0.7% on the day) with aftermarket trading at $170.24.

The muted reaction suggests the results were largely in line with expectations, with investors balancing the earnings decline against record production and continued shareholder returns.

Capital Returns and Balance Sheet

Chevron returned $27.1 billion to shareholders in 2025:

Balance sheet metrics:

The debt increase reflects financing for the Hess acquisition, but leverage remains manageable at 1.0x net debt-to-cash flow.

Segment Performance

Upstream

U.S. upstream earnings declined 11% despite 25% production growth, as lower liquids realizations ($42.99/BBL vs. $53.12/BBL) more than offset volume gains.

International upstream earnings fell 38% due to:

- Unfavorable FX effects (primarily Australia)

- Lower affiliate earnings

- Lower realizations ($57.53/BBL vs. $67.33/BBL)

Downstream

Downstream was a bright spot, with combined earnings of $823 million vs. a loss of $248 million a year ago. The improvement came from higher refined product margins, lower operating expenses, and the absence of prior-year impairments.

U.S. refinery throughput reached the highest level in 20 years, with fewer refineries, due to reliable operations and efficiency improvements.

Key 2025 Achievements

Hess Integration Complete:

- Achieved initial $1 billion synergy target

- Contributed 261 MBOED to 2025 production

Major Project Milestones:

- TCO Future Growth Project started up in Kazakhstan

- Achieved first oil at Yellowtail (4th development in Guyana)

- FID reached on Hammerhead (7th development in Guyana)

- First oil from South N'dola platform in Angola

Strategic Initiatives:

- Expanded exploration acreage by 50%+ vs. 2023

- Entered U.S. lithium sector (Smackover Formation)

- Announced data center power solutions in West Texas

- Achieved $1.5 billion structural cost reductions

Q&A Highlights

TCO Power Issue and Outlook

Management addressed a recent power distribution issue at TCO that temporarily impacted production:

"The team proactively suspended production at the facility when an issue was identified in the power system. Production has been resumed at the Tengiz Field... Full field production capacity not far away."

On debottlenecking, Wirth noted the company has historically improved plant capacity beyond nameplate at TCO and is working on similar improvements for the new project. Full year 2026 guidance of $6 billion of Chevron share free cash flow from TCO at $70 Brent remains unchanged.

Venezuela Expansion Potential

Wirth provided extensive color on Venezuela operations:

"Since 2022, we've grown production by over 200,000 barrels a day. Gross production now is up at around 250,000 barrels a day. And there's the potential for up to an incremental 50% production growth over the next 18-24 months as we get some additional authorizations from the U.S. government."

The activity is entirely self-funded through cash within the ventures, with the potential to bring another 100,000 barrels/day of Venezuelan crude into Chevron's refining system (Pascagoula and El Segundo).

Eastern Mediterranean Growth Story

The Eastern Med represents a major growth engine with over 40 TCF of resource on a gross basis:

"Combined those projects should increase production about 25% and double earnings and cash flow by 2030."

Key projects:

- Tamar: Optimization project adding ~500 million cubic feet/day capacity

- Leviathan: FID taken on expansion to reach 2.1 BCF/day by end of decade

- Aphrodite: Entered FEED, working toward FID in Cyprus

- Egypt: Exploration well planned offshore in underexplored blocks

Permian Capital Efficiency

CFO Bonner highlighted the dramatic improvement in Permian economics:

"We're at $3.5 billion of CapEx already... Since 2022, we've more than doubled our drilling efficiency from that point."

The focus remains on cash flow growth, not production growth, with the Permian held at 1 million BOE/day while driving margin expansion.

Chemical Surfactant Technology

Chevron's proprietary chemical technology is showing strong results:

"We're now realizing 20% improvement in 10-month cumulative recovery on the new wells... we expect that's at least a 10% recovery uplift over the full life of the well."

Treatment rates increased from 40% of new wells in H1 2025 to 85% in 2026, targeting 100% by 2027. Testing is underway in the Bakken, DJ Basin, and Argentina.

Middle East Opportunities

The company signed an MOU in Libya and is engaged in discussions in Iraq:

"We do see a lot of interest in that part of the world, and it's reflected in these more competitive fiscal terms... When we saw President Trump make a visit through the region earlier this year, we saw a notable uptick in inbound inquiries."

Cost Reduction Progress

On the structural cost program, Bonner provided specifics:

"We've saved $1.5 billion thus far on the cost reduction program... The run rate's greater than $2 billion at the end of the year. We're very confident in the target of $3 billion-$4 billion by the end of 2026."

Key drivers include AI integration for supply chain optimization, production chemical optimization across the consolidated shale portfolio, and organizational restructuring.

Forward Outlook

Management highlighted several catalysts for 2026 and beyond:

2026 Production Guidance: 7%-10% growth expected year-over-year, excluding asset sales, driven by:

- Full year of Permian above 1 million BOE/day

- Offshore production up ~200,000 BOE/day from Gulf of Mexico, Guyana, and Eastern Med project startups

- TCO growth of 30,000 BOE/day with optimized maintenance schedule

Key Catalysts:

- Cost reduction target: $3-4 billion in structural cost reductions by end of 2026, with >60% from durable efficiency gains

- Guyana growth: Continued ramp-up at Yellowtail and development of Hammerhead

- TCO optimization: $6 billion Chevron share free cash flow at $70 Brent

- Eastern Mediterranean: Projects to double earnings and cash flow by 2030

- Venezuela: Potential 50% production growth in 18-24 months

- Reserve strength: 158% reserve replacement ratio in 2025, with year-end proved reserves of ~10.6 billion BOE

Balance Sheet Resilience: The company emphasized its portfolio has a dividend and CapEx break-even below $50 Brent with significant debt capacity for flexibility through cycles.

On capital allocation, Wirth summarized: "We've returned more than $100 billion in dividends and buybacks over the last four years. Our track record of growing the dividend is unmatched across decades."

Key Takeaways

Positives:

- Record production of 4,045 MBOED demonstrates successful integration and organic growth

- Strong cash flow of $10.8 billion in Q4 despite price headwinds

- 39th consecutive year of dividend increases

- Hess synergies achieved ahead of schedule

- Downstream turnaround with highest U.S. refinery throughput in 20 years

Concerns:

- Earnings highly sensitive to oil price movements ($64 Brent drove 26% EPS decline)

- Elevated debt levels from Hess acquisition

- International upstream weakness from FX and affiliate earnings

- Lower oil price realizations across all segments

This article has been updated with highlights from Chevron's Q4 2025 earnings call held on January 30, 2026.

Related Links: